If you’re planning to buy a home but don’t have a 20% down payment, you’ve probably heard about Private Mortgage Insurance, or PMI. But how much does PMI really cost, and how will it affect your monthly payments?

Understanding your Private Mortgage Insurance cost is key to knowing the true price of your new home and managing your budget wisely. You’ll learn what factors influence your PMI rates, how to estimate your costs using simple tools, and smart strategies to lower or even avoid PMI altogether.

Keep reading to take control of your mortgage and save money on your path to homeownership.

What Is Private Mortgage Insurance

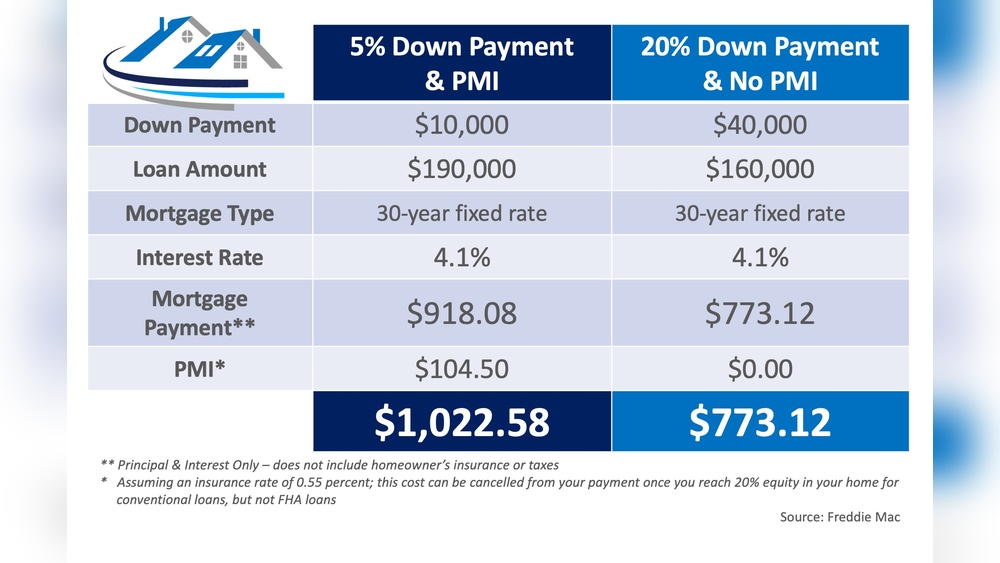

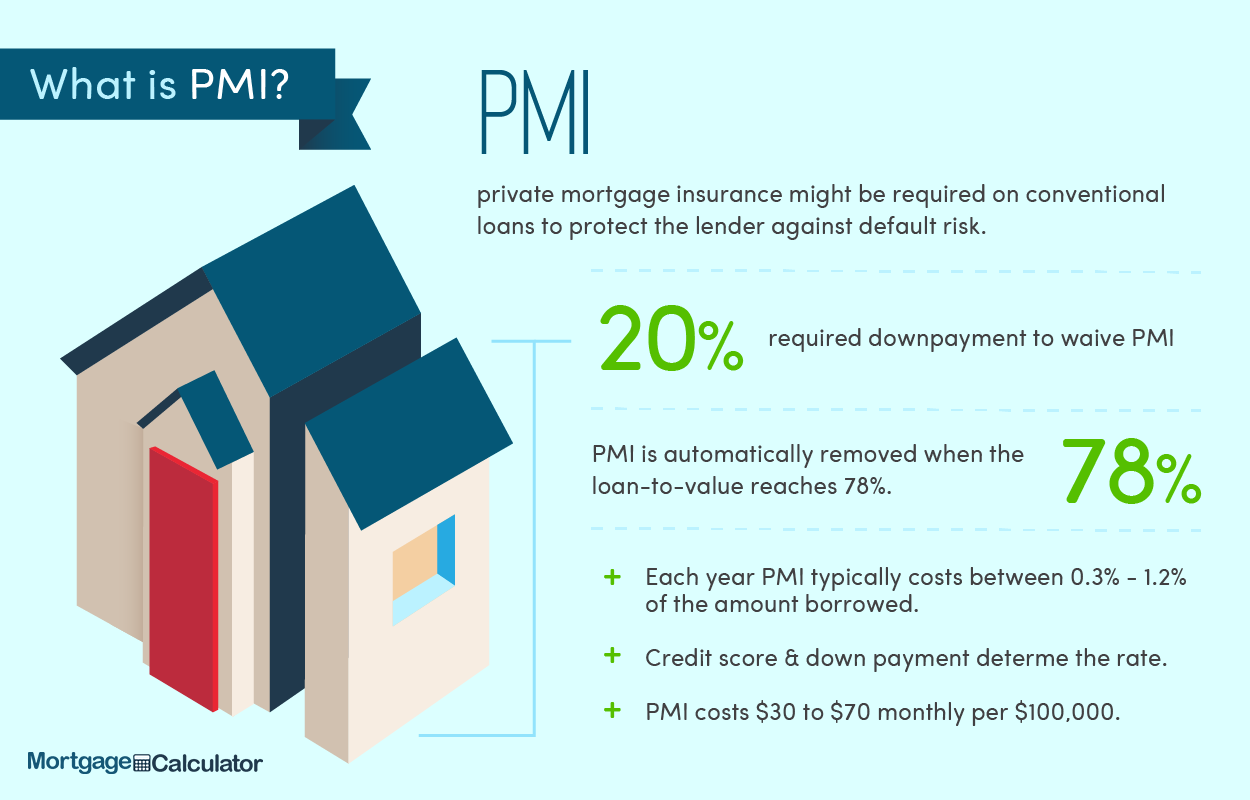

Private Mortgage Insurance (PMI) is an extra cost for homebuyers who pay less than 20% down. It protects the lender if the borrower stops paying the loan. PMI raises your monthly payment but helps you get a loan with a smaller down payment.

The cost of PMI depends on the size of your down payment, your credit score, and the loan type. A bigger down payment means lower PMI costs. Good credit scores also help reduce the price.

Many use online PMI calculators to find out their estimated monthly payment. These tools consider your financial details for a personalized estimate.

How Pmi Costs Are Calculated

PMI cost depends on several key factors. The size of your down payment is crucial. A bigger down payment means lower PMI rates. For example, putting down 20% or more often eliminates PMI altogether.

Credit scores also affect PMI premiums. Higher credit scores lead to lower PMI costs. Lenders see borrowers with good credit as less risky.

The type and amount of your loan matter too. Some loans have higher PMI rates. Larger loan amounts usually mean higher premiums.

| Factor | Effect on PMI Cost |

|---|---|

| Down Payment Size | Higher down payment = Lower PMI cost |

| Credit Score | Better credit score = Lower PMI premium |

| Loan Type and Amount | Different loan types and bigger loans can increase PMI |

Typical Pmi Cost Ranges

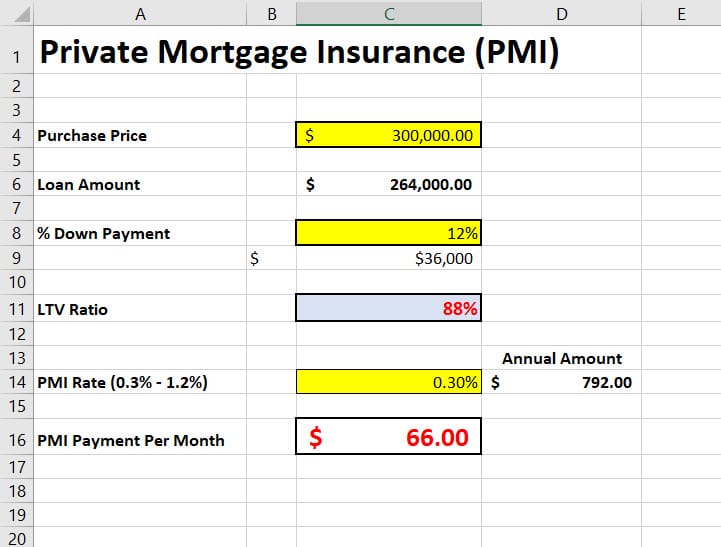

Average monthly premiums for Private Mortgage Insurance (PMI) usually range between 0.3% and 1.5% of the original loan amount annually. This means if your loan is $200,000, you might pay between $50 and $250 per month.

Annual percentage rates for PMI depend on factors like credit score, loan size, and down payment. Higher credit scores and larger down payments usually mean lower PMI rates.

| Loan Program | Typical PMI Cost (Annual %) |

|---|---|

| Conventional Loans | 0.5% – 1.5% |

| FHA Loans | 1.75% (Upfront) + Monthly Premiums |

| VA Loans | No PMI, but Funding Fee Applies |

Different loan programs have varied PMI costs. Conventional loans usually have the lowest monthly premiums. FHA loans require an upfront fee and monthly payments. VA loans do not need PMI but include a funding fee instead.

Using Pmi Calculators

Several popular online tools help estimate PMI costs. Websites like NerdWallet and Credit Karma offer free calculators. These tools ask for basic details such as loan amount, down payment, and credit score. Entering accurate info gives a better estimate of monthly PMI payments.

Customize results by adding your financial details. Include your credit score, loan type, and home price. This helps the calculator adjust PMI rates specifically for your situation. Many calculators also show how different down payment amounts affect PMI costs.

| Factor | Effect on PMI Cost |

|---|---|

| Down Payment | Higher down payment means lower PMI |

| Credit Score | Better score lowers PMI rate |

| Loan Type | Different loans have different PMI costs |

Ways To Lower Pmi Costs

Increasing your down payment reduces PMI costs significantly. A larger down payment lowers the loan amount and the risk for lenders. This often results in a lower PMI rate or no PMI at all if the down payment reaches 20% or more.

Improving credit scores helps lower PMI rates. Higher credit scores show lenders you are less risky. Paying bills on time, reducing debt, and checking credit reports for errors can boost your score. A better score means you pay less for PMI.

Choosing different loan options affects PMI costs. Some loans require PMI only until you reach a certain equity percentage. Others offer lender-paid mortgage insurance, where costs are included in the loan interest rate. Comparing loan types helps find the best PMI deal.

Pmi Payment Methods

Monthly premiums are the most common way to pay PMI. These payments are added to your mortgage bill each month. The amount depends on your loan size and credit score.

Upfront payments require a one-time payment at closing. This option reduces or removes monthly PMI payments. It can save money over time but needs more cash at the start.

Combination plans mix upfront and monthly payments. You pay part of the PMI upfront and the rest monthly. This balances initial cost with ongoing payments.

When And How Pmi Can Be Removed

Reaching 20% equity in your home is the most common way to remove PMI. Once your loan balance drops to 80% of the home’s value, you can ask your lender to cancel PMI. This often requires a home appraisal to confirm your equity.

Refinancing options let you replace your current loan with a new one that may not require PMI. This works well if your home value has increased or you qualify for a better loan. Refinancing can also lower your interest rate.

Automatic cancellation rules protect borrowers by requiring lenders to drop PMI once the loan reaches 78% of the original value. This happens on the loan’s midpoint, but only if payments are current. Lenders must notify you when this happens.

Pmi Vs Other Mortgage Insurance

PMI is private mortgage insurance for conventional loans. FHA mortgage insurance is for government-backed loans. PMI usually costs 0.3% to 1.5% of the loan amount yearly. FHA mortgage insurance has a fixed upfront fee plus monthly payments.

PMI can be canceled once you reach 20% equity in your home. FHA mortgage insurance lasts for the life of the loan if your down payment is less than 10%. PMI costs vary by credit score, loan size, and down payment. FHA insurance costs are mostly fixed regardless of credit score.

| Feature | PMI (Conventional) | FHA Mortgage Insurance |

|---|---|---|

| Cost | 0.3% – 1.5% yearly | Upfront fee + monthly payment |

| Cancellation | Possible at 20% equity | Usually lasts entire loan |

| Based on Credit Score | Yes | No |

| Loan Type | Conventional loans | Government-backed FHA loans |

Common Pmi Myths

Many people think PMI is always expensive. That is not true. The cost depends on your loan size and credit score. Some believe PMI lasts for the entire loan term. Actually, PMI can be removed once you reach 20% equity in your home.

Another myth is that PMI protects the borrower. It actually protects the lender if you stop paying your mortgage. Many think all loans require PMI. Only loans with less than 20% down payment usually need PMI.

Some say PMI rates are fixed. Rates can change based on your financial situation and market conditions. Understanding these facts helps you make better decisions about your mortgage.

Pmi Insights For Austin, Texas Buyers

Private Mortgage Insurance (PMI) in Austin usually costs 0.5% to 1% of the loan amount per year. This means a $300,000 loan might have a PMI cost of $1,500 to $3,000 annually. The down payment size greatly affects PMI rates. A larger down payment lowers the PMI cost. Credit score is another key factor; higher scores get better rates.

Local market trends in Austin also influence PMI. Rising home prices can mean higher loan amounts, which may increase PMI costs. Different lenders may offer varying PMI rates, so it pays to compare. Many buyers use online PMI calculators to estimate costs based on their own numbers.

:max_bytes(150000):strip_icc()/dotdash-whats-difference-between-private-mortgage-insurance-pmi-and-mortgage-insurance-premium-mip-Final-fc26360e02cc4b30af01326412b49cf0.jpg)

Frequently Asked Questions

How Much Is Pmi On A $300,000 Home?

PMI on a $300,000 home typically ranges from 0. 5% to 1% annually of the loan amount. This means $1,250 to $2,500 per year, or about $104 to $208 monthly. Exact costs depend on your down payment, credit score, and lender policies.

Use a PMI calculator for precise estimates.

Does Pmi Go Away After You Reach 20%?

PMI usually stops once your loan balance reaches 78% of the home’s original value. You can request cancellation at 80%.

How Much Is Pmi On A $100,000 Loan?

PMI on a $100,000 loan usually ranges from 0. 3% to 1. 5% annually. This means $300 to $1,500 yearly. Exact costs depend on credit score, down payment, and loan type. Use online PMI calculators for personalized estimates.

How Much Is Mortgage Insurance On A $500,000 Loan?

Mortgage insurance on a $500,000 loan typically costs 0. 3% to 1. 5% annually. This equals $1,500 to $7,500 per year. Exact rates depend on credit score, down payment, and loan type. Use online PMI calculators for personalized estimates.

Conclusion

Private Mortgage Insurance costs vary based on several factors. Your down payment size and credit score influence the premium. Using online PMI calculators helps estimate your specific costs. Understanding these expenses aids in better budgeting for your home loan. Remember, PMI protects lenders when your down payment is low.

Paying attention to PMI can save money over time. Keep learning about mortgage terms to make smart financial choices.

Read More

- No Obligation Mortgage Quote: Get Fast, Free, and Easy Offers Today

- Best Mortgage Lender Quotes: Unlock Top Rates & Save Big Today

- Home Loan Quote Calculator: Instantly Compare Rates & Save Big

- Online Mortgage Quote Comparison: Unlock Best Rates Fast

- Instant Mortgage Rate Quote: Unlock Your Best Home Loan Today

- First Time Buyer Mortgage Broker: Expert Tips for Easy Approval

- Independent Mortgage Advisor Cost: What You Need to Know Today

- Mortgage Broker Fees UK: What You Need to Know Before Applying

- Online Mortgage Broker Comparison: Find the Best Rates Fast

- Self Employed Mortgage Qualification: Expert Tips to Secure Approval