Buying a home is one of the biggest commitments you’ll make, and your mortgage is likely your largest monthly expense. But have you thought about what would happen to your mortgage if something unexpected happened to you?

That’s where life insurance for your mortgage steps in. It’s designed to protect your family from the stress of mortgage payments if you’re no longer around. You’ll discover how mortgage life insurance works, the pros and cons, and whether it’s the right choice for your financial peace of mind.

Keep reading to make sure your home—and your family’s future—stay secure no matter what.

Mortgage Life Insurance Basics

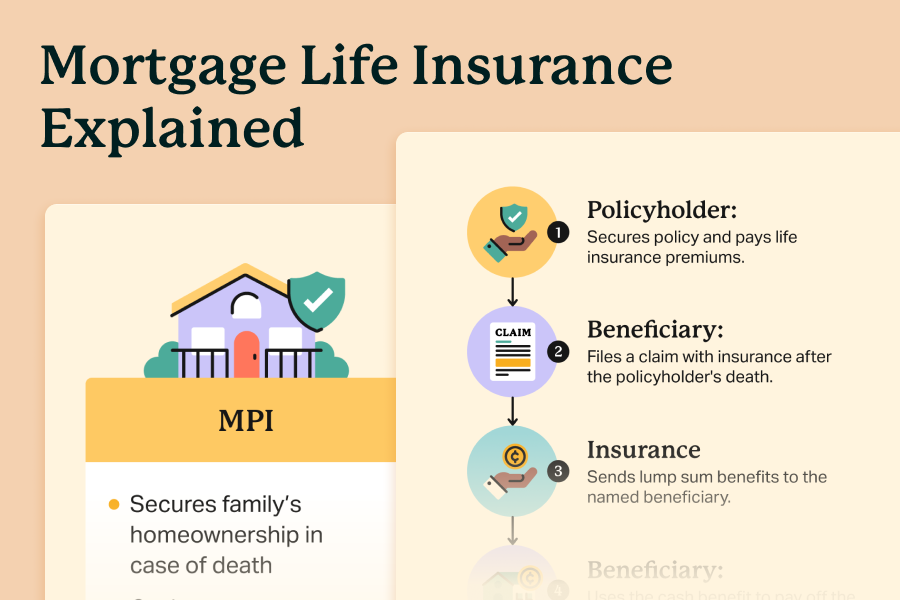

Mortgage life insurance helps pay off your home loan if you die. It works by linking a life insurance policy to your mortgage balance. The payout decreases as you pay down your mortgage. This means the coverage drops over time, matching what you still owe.

Some policies have added riders. These riders can help if you become seriously ill, disabled, or lose your job without choice. They may cover mortgage payments during tough times. This gives you extra protection beyond just death benefits.

These riders often include:

- Critical illness coverage

- Disability protection

- Unemployment benefits

Such options can make mortgage life insurance more flexible and helpful when facing unexpected life events.

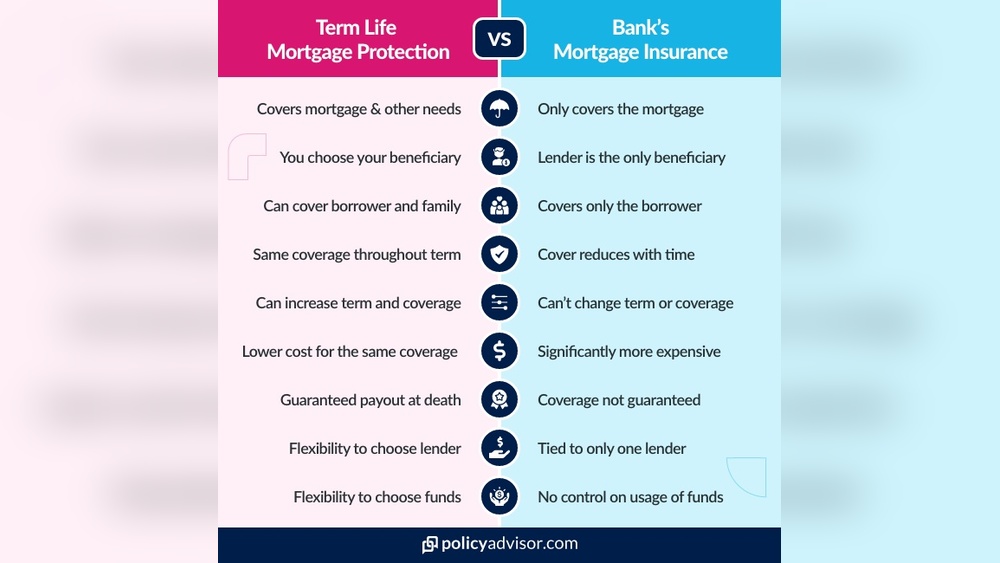

Mortgage Insurance Vs Life Insurance

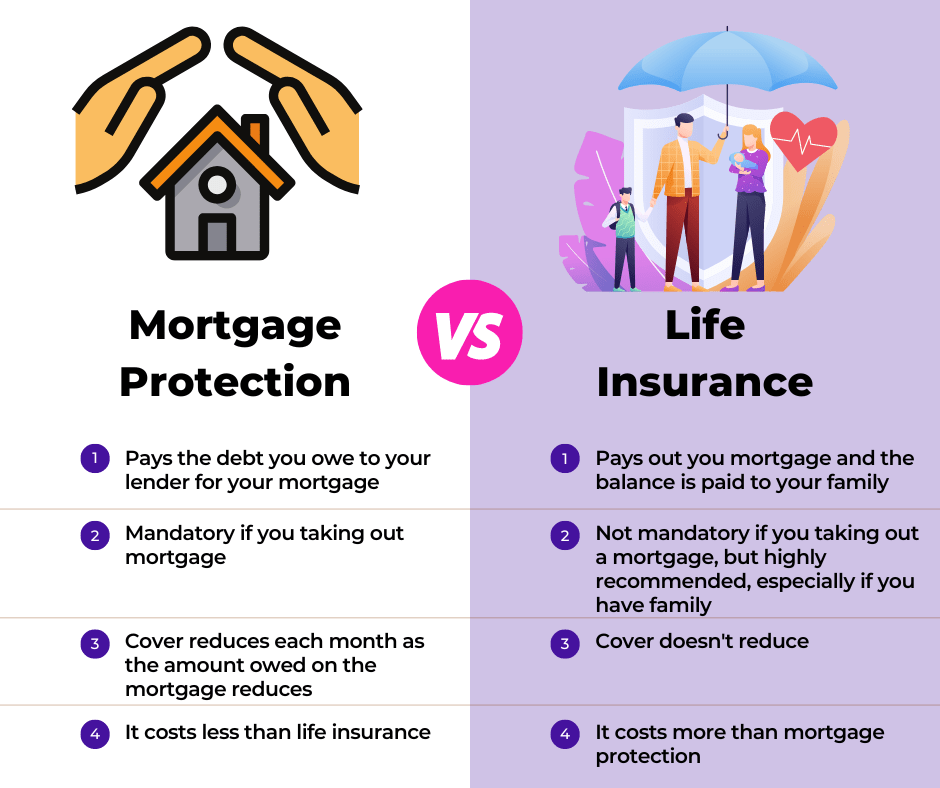

Mortgage insurance pays off your home loan if you can’t. It is tied directly to your mortgage balance. The payout goes only to the lender, not your family.

Life insurance offers more flexibility. It pays a set amount to your loved ones, who decide how to use it. The money can cover mortgage, bills, or other needs.

| Feature | Mortgage Insurance | Life Insurance |

|---|---|---|

| Payout Recipient | Mortgage lender | Your beneficiaries |

| Coverage Amount | Decreases with loan balance | Fixed amount chosen by you |

| Use of Funds | Only for mortgage payoff | Any purpose your family needs |

| Approval | Usually easier, no medical exam | May require health check |

Choosing depends on what matters most. If you want simple coverage for your home loan, mortgage insurance fits. If you want protection for your family’s broader needs, life insurance works better.

Benefits Of Mortgage Life Insurance

Easy approval makes mortgage life insurance a good choice for many. It often does not require medical exams. This helps people with health problems get coverage. The process is quick and simple.

Mortgage debt coverage means the insurance pays off the home loan. This protects your family from losing the house if something happens to you. The payout goes directly to the lender, clearing the debt.

These features give peace of mind. Families can focus on healing instead of worrying about payments. It keeps the home safe and secure during tough times.

Drawbacks To Consider

Strict payout restrictions mean the money goes only to the mortgage. Families cannot use the funds for other needs like funeral expenses or daily bills. This limits the flexibility of the payout.

Declining coverage value is common. The payout amount often decreases as the mortgage balance lowers. This can leave less money available if the insured dies late in the policy term.

Many policies have fixed premiums. You pay the same amount every month even though the coverage amount goes down. This can feel unfair since the benefit shrinks but the cost stays the same.

Cost Factors

Typical premiums for mortgage life insurance vary widely. Age, health, and coverage amount play big roles. Younger and healthier people usually pay lower rates. Coverage that matches the mortgage balance costs more. Term length also affects price; longer terms mean higher premiums.

Factors influencing price include:

- Age: Older applicants pay more due to higher risk.

- Health: Better health means lower premiums.

- Coverage amount: More coverage increases cost.

- Policy term: Longer terms raise the price.

- Type of policy: Term life usually costs less than whole life.

Insurance companies also consider lifestyle, such as smoking or risky jobs. Some offer discounts for good health or no smoking. Shopping around helps find the best price for your needs.

Alternatives To Mortgage Life Insurance

Term life insurance offers coverage for a set time, like 10 or 20 years. It usually costs less than mortgage life insurance. You can choose the amount that fits your needs. The payout goes to your family, who can use it for anything, not just the mortgage.

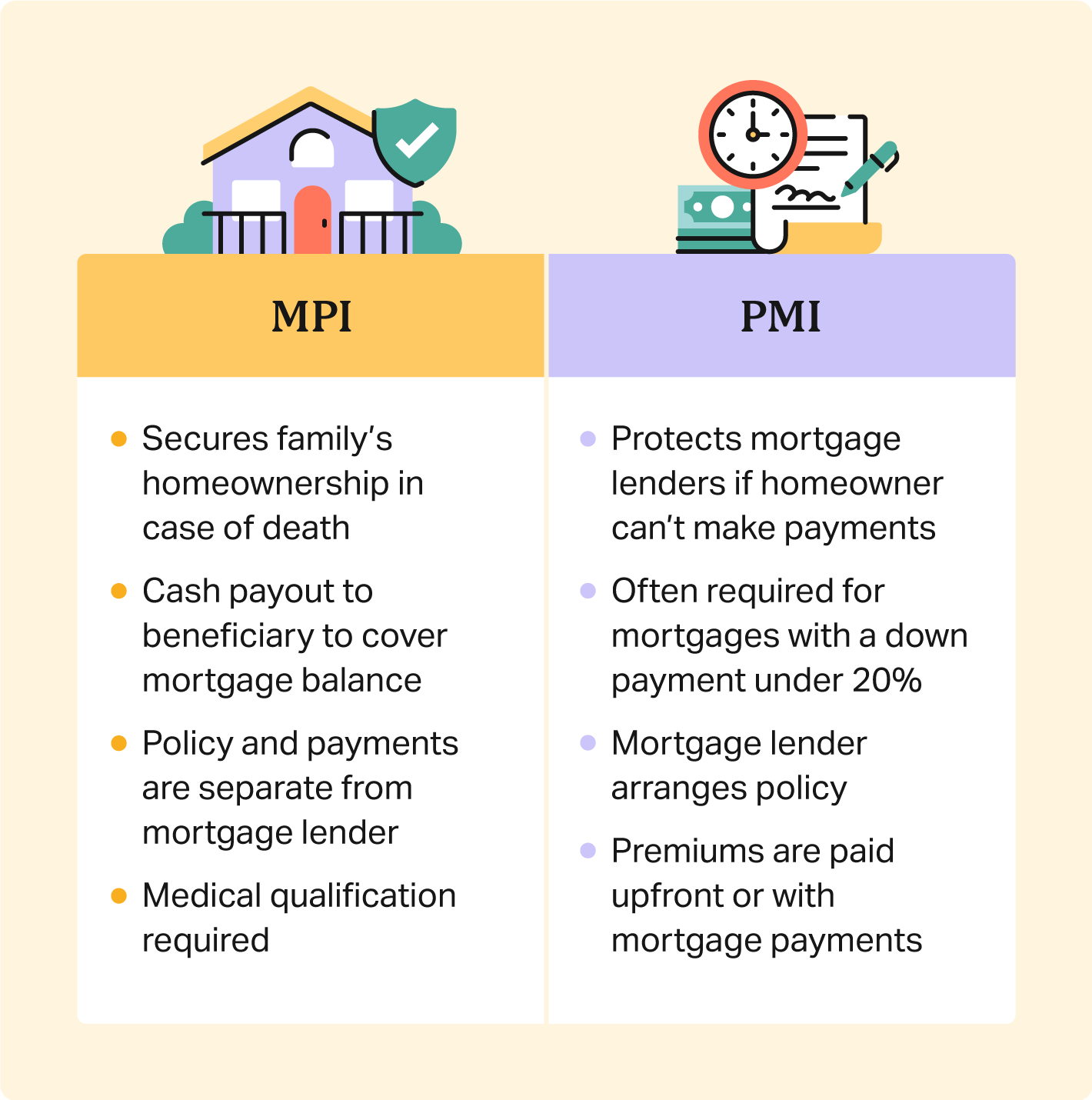

Private mortgage insurance (PMI) protects the lender, not you. It is required if your down payment is less than 20%. PMI stops once you have enough equity in your home. It does not provide money to your family if you die.

Other options include disability insurance and critical illness insurance. These help cover mortgage payments if you cannot work. Combining different protections can offer better peace of mind.

Choosing The Right Policy

Assessing your financial situation helps find the best policy for mortgage life insurance. Start by listing all your debts, income, and monthly expenses. This gives a clear view of what your family might need if something happens to you.

Evaluating coverage needs means deciding how much insurance will cover your mortgage balance. Think about future changes like interest rates or extra payments. It is smart to choose a policy that covers the full mortgage amount to keep your family safe.

Consulting with professionals like insurance agents or financial advisors provides expert advice. They can explain different policies and help find one that fits your budget and needs. Talking to experts ensures you understand all options clearly.

Local Options In Austin, Texas

Austin, Texas has several trusted life insurance providers for mortgage protection. Local companies often understand Texas-specific rules better. Some top providers include State Farm, Allstate, and Farmers Insurance. These companies offer policies that cover the mortgage balance if the borrower passes away.

Texas requires life insurance policies to follow state regulations. These rules protect consumers and ensure transparency. For example, policies must clearly state payout terms and exclusions. Some policies also allow adding riders for disability or critical illness coverage.

| Provider | Key Features | State Compliance |

|---|---|---|

| State Farm | Flexible terms, customizable riders | Fully compliant with Texas regulations |

| Allstate | Easy application, quick approval | Meets all state insurance laws |

| Farmers Insurance | Comprehensive coverage, local agents | Adheres to Texas insurance standards |

Frequently Asked Questions

Is Mortgage Life Insurance Worth It?

Mortgage life insurance can help pay off your mortgage if you pass away, but it often costs more and offers less flexibility than term life insurance. Consider your family’s financial needs before choosing.

Can You Have Life Insurance On A Mortgage?

Yes, you can have life insurance on a mortgage. It pays off your mortgage balance if you die during the policy term.

Can I Get Life Insurance If I Have Cirrhosis?

Yes, you can get life insurance with cirrhosis, but options may be limited and premiums higher. Approval depends on cirrhosis severity and overall health. Some insurers offer high-risk or graded policies. Consulting specialized agents improves chances of finding suitable coverage.

How Much Does Mortgage Life Insurance Typically Cost?

Mortgage life insurance typically costs between $20 and $50 per month, depending on age, health, and mortgage amount.

Conclusion

Choosing life insurance for your mortgage helps protect your family’s home. It ensures mortgage payments get covered if you pass away. This can prevent financial strain during tough times. Compare policies carefully to find the best fit. Consider how much coverage you need and the premium costs.

Life insurance offers peace of mind and financial security. It supports your loved ones when they need it most. Taking action now can safeguard your family’s future. Simple steps today lead to a safer tomorrow.

Read More

- No Obligation Mortgage Quote: Get Fast, Free, and Easy Offers Today

- Best Mortgage Lender Quotes: Unlock Top Rates & Save Big Today

- Home Loan Quote Calculator: Instantly Compare Rates & Save Big

- Online Mortgage Quote Comparison: Unlock Best Rates Fast

- Instant Mortgage Rate Quote: Unlock Your Best Home Loan Today

- First Time Buyer Mortgage Broker: Expert Tips for Easy Approval

- Independent Mortgage Advisor Cost: What You Need to Know Today

- Mortgage Broker Fees UK: What You Need to Know Before Applying

- Online Mortgage Broker Comparison: Find the Best Rates Fast

- Self Employed Mortgage Qualification: Expert Tips to Secure Approval