If you’re a homeowner or planning to become one, understanding how homeowners insurance and mortgage escrow work together can save you money and stress. You might have heard these terms before but aren’t quite sure how they impact your monthly payments or protect your investment.

Knowing the role of homeowners insurance in your mortgage escrow account helps you avoid surprises and keeps your home safe from unexpected costs. Stick with me, and I’ll break down everything you need to know in simple terms so you can feel confident about your home’s financial safety net.

Mortgage Escrow Basics

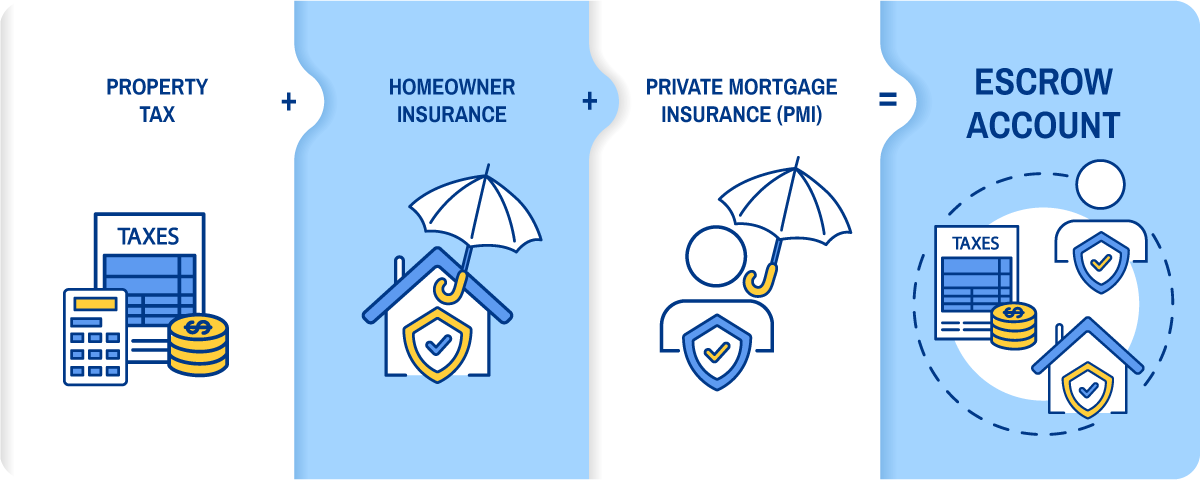

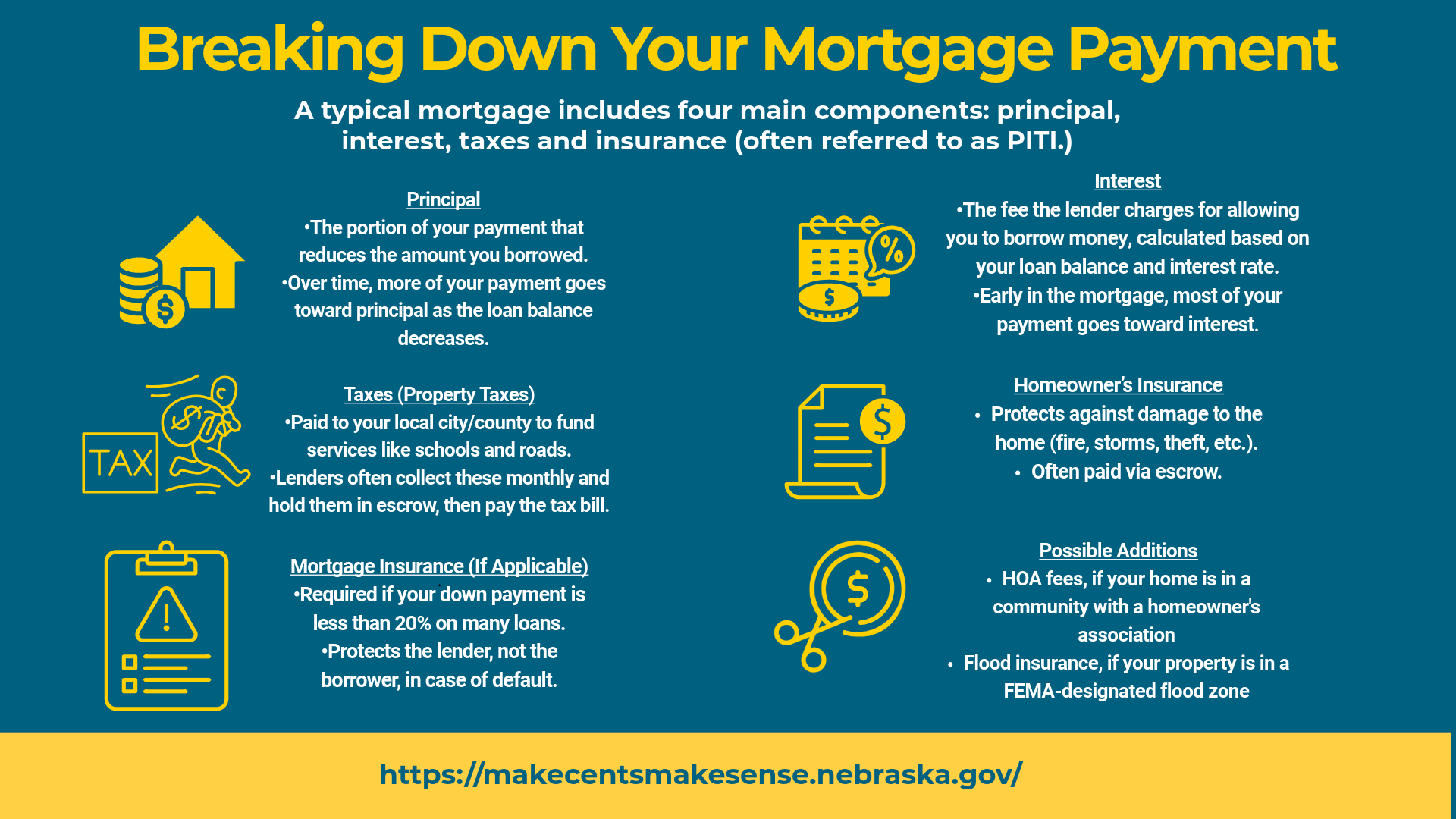

An escrow account is a special bank account used to hold money for home expenses. It helps with homeowners insurance and property taxes. Each month, a part of the mortgage payment goes into this account. The lender uses this money to pay the insurance and taxes on time.

Escrow protects both the homeowner and the lender. It ensures insurance premiums are paid without delay. The lender wants to keep the home safe and legally protected. If insurance or taxes are not paid, the lender may pay them from escrow and charge the homeowner.

| Why Lenders Require Escrow |

|---|

| Ensures insurance payments are made on time |

| Protects the property from loss or damage |

| Keeps taxes current to avoid legal issues |

| Helps homeowners budget for large expenses |

Homeowners Insurance And Escrow

Homeowners insurance covers your house and belongings from damage and theft. It usually includes dwelling protection, personal property coverage, and liability protection. Some policies also cover additional living expenses if you must stay elsewhere during repairs.

Annual premiums are paid to keep the insurance active. These payments can be made directly or through an escrow account. An escrow account collects money monthly with your mortgage payment to cover insurance and taxes. This helps spread out the cost over the year.

Insurance amounts can change based on factors like property value or risk. The escrow account adjusts accordingly. Lenders review and update escrow payments yearly to match new insurance costs. This process avoids large bills or missed payments.

Managing Your Escrow Account

Tracking escrow payments helps you know where your money goes. Your mortgage lender collects money monthly. This pays for property taxes, homeowners insurance, and sometimes other fees. Keep an eye on your statements to avoid surprises.

Escrow analysis happens yearly. The lender checks if enough money is in your account. If there is extra money, called a surplus, you may get a refund or lower payments next year.

Shortages happen when not enough money is collected. The lender may ask for a payment to cover the gap. Or, they might increase your monthly escrow payment to avoid future shortages.

Saving Money On Insurance Escrow

Choosing the right homeowners insurance can save you money on your escrow. Look for policies that offer good coverage at a fair price. Some companies provide discounts for safety features like alarms or smoke detectors.

Shopping around for better rates is smart. Different insurers charge different prices. Compare quotes from several companies before deciding. Even small savings can add up over time.

Bundling insurance policies means buying home and auto insurance from the same company. This often leads to lower overall costs. Ask your agent about bundling options to reduce your escrow payments.

Escrow Account Tips For Homeowners

Requesting escrow waivers lets some homeowners avoid escrow accounts. Not all lenders allow this. Usually, you need a strong credit score and enough equity in your home. Waivers can lower your monthly payments but increase risk. You must pay taxes and insurance yourself if waived.

Communicating with your lender helps keep escrow accounts clear. Ask questions about your balance and payments. Report any changes in insurance or taxes quickly. Stay in touch to avoid surprises or errors.

Reviewing annual escrow statements is very important. These statements show money collected and paid out. Check for mistakes like overpayments or shortages. Contact your lender if something looks wrong. This helps keep your account accurate and up to date.

Common Escrow Issues And Solutions

Unexpected premium increases can surprise homeowners. This often happens due to changes in insurance rates or property value. To handle this, review your escrow account statement carefully. Contact your mortgage lender to discuss options like adjusting your monthly payments.

Errors in escrow payments may occur. These can be due to miscalculations or delayed payments. Keep track of your payments and compare them to your mortgage statements. Report any mistakes to your lender promptly to avoid late fees or coverage gaps.

Refinancing your mortgage affects your escrow account. The new loan terms may change your payment amounts. Inform your insurance company and lender about refinancing. Make sure escrow funds are updated to match your new mortgage agreement.

Local Considerations In Austin, Texas

Texas state laws require homeowners insurance to protect homes and lenders. Austin has specific rules that affect escrow accounts tied to mortgages. These rules help ensure insurance payments are made on time through escrow.

The Austin housing market shows steady growth, which can raise insurance costs. Rising home values mean higher premiums. Escrow accounts must adjust to cover these changes.

Local resources help Austin homeowners manage insurance and escrow. City websites and local insurance agents provide guidance. They explain how to keep escrow balances correct and avoid surprises at renewal.

Frequently Asked Questions

Is It Homeowner Or Home Owner?

Use “homeowner” as one word in almost all cases. Avoid “home owner” or “home-owner” unless a style guide requires it.

Is Homeowners 1 Or 2 Words?

“Homeowners” is one word. Use it as a single term in most contexts, including insurance and associations. Avoid splitting it into two words.

What Does “homeowners” Mean?

“Homeowners” means individuals who own and live in their residential property. They hold legal rights to the home.

Is It Homeowner’s Or Homeowners?

Use “homeowner’s” to show singular possession (one homeowner owns). Use “homeowners” for the plural form (multiple owners). For plural possession, use “homeowners’. ” Choose based on whether you mean one owner, many owners, or possession by multiple owners.

Conclusion

Understanding homeowners insurance and mortgage escrow can protect your home and finances. Escrow accounts help manage your insurance payments smoothly. This setup ensures your coverage stays active without missed payments. Knowing how escrow works gives you control and peace of mind.

Review your escrow statements regularly to avoid surprises. Clear knowledge helps you make smart decisions about your home. Protecting your investment starts with understanding these key details. Keep your home safe and your payments on track.

Read More

- No Obligation Mortgage Quote: Get Fast, Free, and Easy Offers Today

- Best Mortgage Lender Quotes: Unlock Top Rates & Save Big Today

- Home Loan Quote Calculator: Instantly Compare Rates & Save Big

- Online Mortgage Quote Comparison: Unlock Best Rates Fast

- Instant Mortgage Rate Quote: Unlock Your Best Home Loan Today

- First Time Buyer Mortgage Broker: Expert Tips for Easy Approval

- Independent Mortgage Advisor Cost: What You Need to Know Today

- Mortgage Broker Fees UK: What You Need to Know Before Applying

- Online Mortgage Broker Comparison: Find the Best Rates Fast

- Self Employed Mortgage Qualification: Expert Tips to Secure Approval