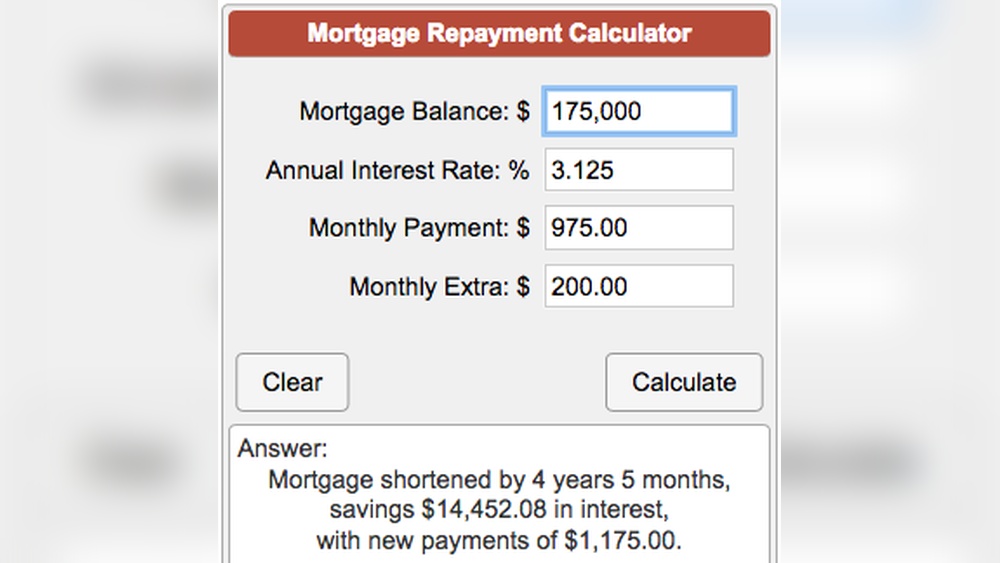

Thinking about buying a home? One of the first questions you probably have is: How much will my monthly mortgage payment be?

That’s where a Home Loan Quote Calculator becomes your best friend. This simple tool puts you in control by giving you a clear estimate of your monthly payments, including principal, interest, taxes, and insurance. Imagine knowing exactly what to expect before you even start house hunting.

With a few easy inputs, you can see how different loan amounts, interest rates, and down payments affect your budget. Keep reading to discover how using a Home Loan Quote Calculator can save you money, reduce stress, and help you make smarter decisions on your path to homeownership.

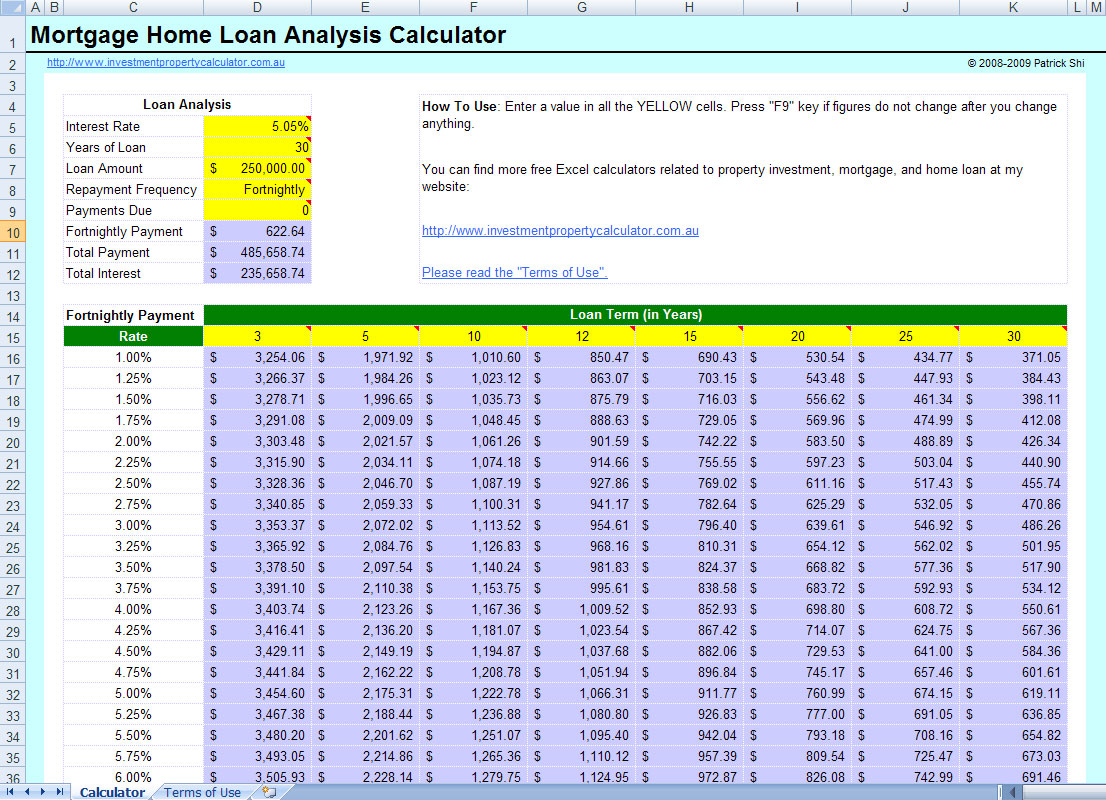

How Home Loan Calculators Work

The fixed-rate mortgage formula helps calculate your monthly payments. It uses the loan amount, interest rate, and loan term. The formula ensures you pay the same amount every month.

Here is the basic formula:

| Variable | Description |

|---|---|

| M | Monthly payment |

| P | Loan principal (amount borrowed) |

| r | Monthly interest rate (annual rate ÷ 12) |

| n | Total number of monthly payments (loan term in months) |

The formula calculates M as:

M = P × [r(1 + r)n] / [(1 + r)n − 1]

This method helps predict your principal and interest costs each month. It does not include taxes or insurance.

Essential Details For Accurate Quotes

Home price directly affects your loan amount and monthly payments. A higher price means a bigger loan and larger payments. Lower home prices reduce what you borrow and your monthly costs.

Interest rate determines how much extra you pay on the loan. Even a small increase in rate raises your monthly payment a lot. Rates depend on the market, your credit score, and loan type.

Both factors work together. For example, a low price with a high rate may cost the same as a high price with a low rate. Understanding these helps you get a more accurate home loan quote.

Accounting For Additional Costs

Property taxes add a big cost to your monthly payments. They are usually a percentage of the home’s value and can change by location. Homeowners insurance protects your home from damage. Lenders require it to keep your loan safe. HOA fees apply if your home is in a community with shared spaces. These fees cover maintenance and community services.

All these costs add up. They should be included in your monthly budget. This helps you know the full price of owning a home. Use a home loan quote calculator that includes these costs. It gives a clearer picture of what you will pay every month.

Comparing Loan Rates Instantly

Online loan calculators help you compare rates instantly. Enter your loan amount, term, and interest rate to see monthly payments. These tools show principal and interest costs clearly.

Multiple quotes let you find the best loan deal. Different lenders offer varying rates and fees. Comparing helps you save money over time.

Benefits include:

- Faster decisions by seeing all options at once.

- Clear cost breakdowns with taxes and insurance included.

- Better budgeting with accurate monthly payment estimates.

- More negotiating power with lender quotes in hand.

Using online calculators is simple and free. Just input your details and get instant results. This makes home buying easier and less stressful.

Maximizing Savings With Quotes

Negotiating better rates can significantly lower your monthly payments. Always compare multiple quotes to find the best deal. Lenders may offer different rates based on your credit score and loan amount. Don’t hesitate to ask for a lower rate or better terms. Small rate differences add up to big savings over time.

Identifying hidden fees is key to understanding the true cost of your home loan. Some fees may not be obvious at first glance, such as origination fees, processing fees, or prepayment penalties. Carefully review the loan estimate and ask your lender to explain any unclear charges. Being aware of these costs helps avoid surprises later.

Tools To Check Home Affordability

Income and debt play a big role in home affordability. Lenders check your monthly income to see how much you can repay. They also look at your existing debts, like credit cards or car loans. A lower debt means you can borrow more for a home.

Popular calculators like Bankrate and Zillow help estimate how much house you can afford. These tools include principal, interest, taxes, and insurance. Some even add HOA fees if you buy a condo or planned community home.

| Calculator | Key Features |

|---|---|

| Bankrate Mortgage Calculator | Breaks down monthly payments by principal, interest, taxes, insurance |

| Zillow Mortgage Calculator | Includes HOA fees and offers quick affordability estimates |

| Wells Fargo Home Affordability Calculator | Considers income, debts, and other financial details |

Tips For Using Loan Calculators Effectively

Always enter correct loan details into the calculator. This includes the loan amount, interest rate, and loan term. Small errors can lead to big differences in the estimated payment.

Keep the interest rates updated. Rates change often. Use the latest rates to get a realistic estimate. Check trusted sites or your lender for current rates.

Remember, a loan calculator only provides an estimate. It does not include all possible fees or costs. Use it as a starting point, not a final answer.

Frequently Asked Questions

Can A 70 Year Old Woman Get A 30-year Mortgage?

A 70-year-old woman can get a 30-year mortgage if she meets lender criteria. Approval depends on income, credit, and financial stability. Some lenders may prefer shorter terms or higher down payments for older borrowers. Always compare options and consult with mortgage professionals.

How Much Is A $500,000 Mortgage At 6% Interest?

A $500,000 mortgage at 6% interest has a monthly principal and interest payment of about $3,000 on a 30-year term.

What Is The 3 7 3 Rule In Mortgage?

The 3-7-3 rule in mortgage means a loan must be approved within 3 days, close within 7 days, and fund within 3 days after closing.

What Salary Do You Need For A $400,000 Mortgage?

To afford a $400,000 mortgage, you typically need an annual salary of around $100,000 to $120,000. This estimate assumes a 4% interest rate and a 30-year term. Lenders prefer your monthly housing costs not to exceed 28% to 31% of your gross income.

Conclusion

Using a home loan quote calculator helps you plan your budget better. It shows monthly payments and extra costs clearly. You can compare different loan options easily. This tool saves time and reduces guesswork. Try it to understand what fits your finances best.

Making informed choices leads to less stress in home buying. A simple step that brings clarity and confidence. Keep your goals in sight and use the calculator often.

Read More

- No Obligation Mortgage Quote: Get Fast, Free, and Easy Offers Today

- Best Mortgage Lender Quotes: Unlock Top Rates & Save Big Today

- Online Mortgage Quote Comparison: Unlock Best Rates Fast

- Instant Mortgage Rate Quote: Unlock Your Best Home Loan Today

- First Time Buyer Mortgage Broker: Expert Tips for Easy Approval

- Independent Mortgage Advisor Cost: What You Need to Know Today

- Mortgage Broker Fees UK: What You Need to Know Before Applying

- Online Mortgage Broker Comparison: Find the Best Rates Fast

- Self Employed Mortgage Qualification: Expert Tips to Secure Approval

- Home Loan Approval Requirements: Essential Tips for Fast Approval